For companies in the business of lending money, Interest Revenues are reported in the operating section of the multiple-step income statement. Under the accrual basis of accounting, the Service Revenues account reports the fees earned by a company during the time period indicated in the heading of the income statement. Service Revenues is an operating revenue account and will appear at the beginning of the company’s income statement. As noted earlier, expenses are almost always debited, so we debit Wages Expense, increasing its account balance. Since your company did not yet pay its employees, the Cash account is not credited, instead, the credit is recorded in the liability account Wages Payable.

What is an example of a contra revenue account?

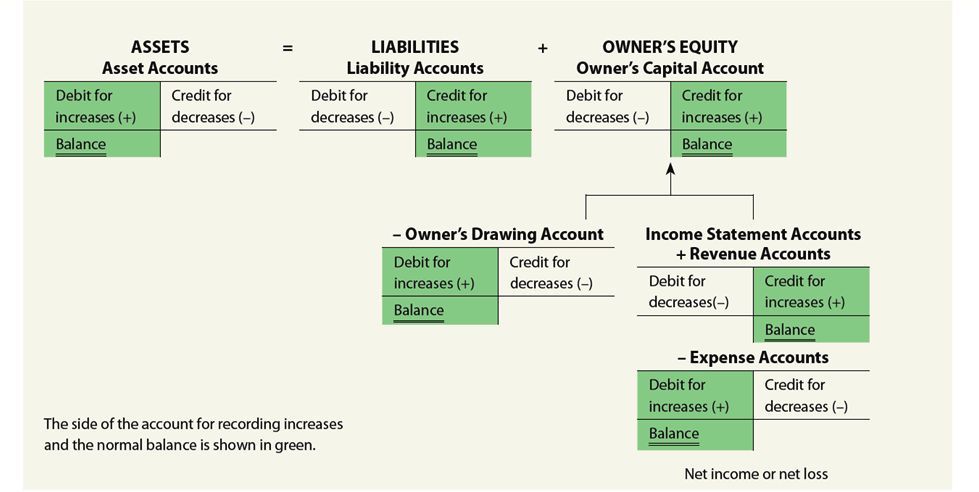

The purpose of the Owner’s Withdrawal account is to track the amounts taken out of the business without impacting the balance of the original equity account. Accounts Receivable is an asset account and is increased with a debit; Service Revenues is increased with a credit. These accounts facilitate auditing and financial analysis by providing a detailed breakdown of adjustments made during a specific accounting period. This information assists auditors, and financial analysts in evaluating a company’s financial performance and risk exposure. When the company pays the cost of having the flyer printed, a journal entry is done.

Income Statement

The gain is the difference between the proceeds from the sale and the carrying amount shown on the company’s books. This means that the new accounting year starts with no revenue amounts, no expense amounts, and no amount in the drawing account. A contra account is a type of account that is used to offset another account. It is a separate account that is linked to another account, and it is used to reflect the opposite of the balance in that account.

Contra Revenue Accounts

Allowance for obsolete inventory or obsolete inventory reserve are also examples of contra asset accounts. Sales returns is a contra revenue account as the figure is a negative amount net against total sales revenue. It would appear on the company’s income statement in the revenue section. The contra revenue accounts commonly used in small-business accounting include sales returns, sales allowance and sale discounts.

Double Entry Bookkeeping

They also help to provide a clear picture of a company’s financial health and performance. In accounting, a contra account is a general ledger account that offsets the balance of another general ledger account. A contra account the usual balance in a contra-revenue account is a: is used to reduce the value of an asset or liability account, which results in a net balance that reflects the true value of the account. Accumulated depreciation is used to offset the balance of a fixed asset account.

Cash Flow Statement

- If a contra account is not used, it can be difficult to determine historical costs, which can make tax preparation more difficult and time-consuming.

- This means that the new accounting year starts with no revenue amounts, no expense amounts, and no amount in the drawing account.

- They are used to provide transparency in accounting by showing adjustments or reductions made to certain accounts.

- The contra revenue accounts commonly used in small-business accounting include sales returns, sales allowance and sale discounts.

- Therefore, the net amount of the accounts receivable that is expected to turn to cash is $38,000.

Accumulated depreciation reflects the reduction in value of a fixed asset. There are several types of contra accounts, including accumulated depreciation, allowance for doubtful accounts, and sales returns and allowances. Each type of contra account represents a different aspect of a company’s financial position. A contra revenue account carries a debit balance and reduces the total amount of a company’s revenue. The amount of gross revenue minus the amount recorded in the contra revenue accounts equal a company’s net revenue.

Whereas assets normally have positive debit balances, contra assets, though still reported along with other assets, have an opposite type of natural balance. Transactions that involve contra accounts are recorded in the general ledger, which is a record of all financial transactions made by a company. The general ledger is used to create financial statements such as the balance sheet and income statement. Discount on bonds payable is a contra liability account that is used to offset the balance of the bonds payable account. It represents the amount of discount that was given when the bonds were issued.

Permanent accounts are not closed at the end of the accounting year; their balances are automatically carried forward to the next accounting year. It is linked to specific accounts and is reported as reductions from these accounts. The allowance method of accounting allows a company to estimate what amount is reasonable to book into the contra account. The percentage of sales method assumes that the company cannot collect payment for a fixed percentage of goods or services that it has sold. The purpose of a contra account is to offset the balance of a related account. Contra accounts are an essential part of accounting that are often misunderstood or overlooked.

Contra revenue accounts are used to offset the balance in a revenue account. For example, if a company has a revenue account for sales returns and allowances, they would also have a contra revenue account to offset the balance in the sales returns and allowances account. For example, a contra account to accounts receivable is a contra asset account. This type of account could be called the allowance for doubtful accounts or bad debt reserve.

It represents the amount of discount that was given when the notes were issued. The purpose of this account is to increase the effective interest rate of the notes. Treasury stock is a contra equity account that is used to offset the balance of the common stock account. It represents the amount of stock that has been repurchased by the company. The purpose of this account is to reduce the total equity on the balance sheet. By using contra accounts, companies can provide a more accurate representation of their financial position in their financial statements.