Since budgets come with inevitable variances, an alternative method is desired. An alternative method is to follow the cost-volume-profit or the CVP approach. Our blog post goes beyond just explaining what target profit is; we’ll provide a practical guide designed to navigate through its calculation effortlessly. And with real-life examples backing up our advice, you’re sure to grasp the concepts more readily. Target Profit is the estimated amount of profit the management hopes to achieve during an accounting period and is forecasted and updated regularly as per the business’s progress.

Target Net Income Formula

Generally the above calculation is fine providing the business has the production capacity to produce 9,091 units and the target market is large enough accommodate them. If not, then the formula can be used to change any of the three parameters fixed costs, selling price, or product cost in order to reduce the number of units to an appropriate level. To determine the number of units required to achieve this target profit after taxes, we can use the same formula we employed earlier.

Target Profit Calculation Process

Here are a few advantages of using the target profit approach as compared to the arbitrary budgeting method. Target profit and cost-volume-profit analysis combined can offer useful information to the management for decision-making in the long term. An alternative method using the weighted average cost to sales (C/S) ratio can be used to determine the target profit as well.

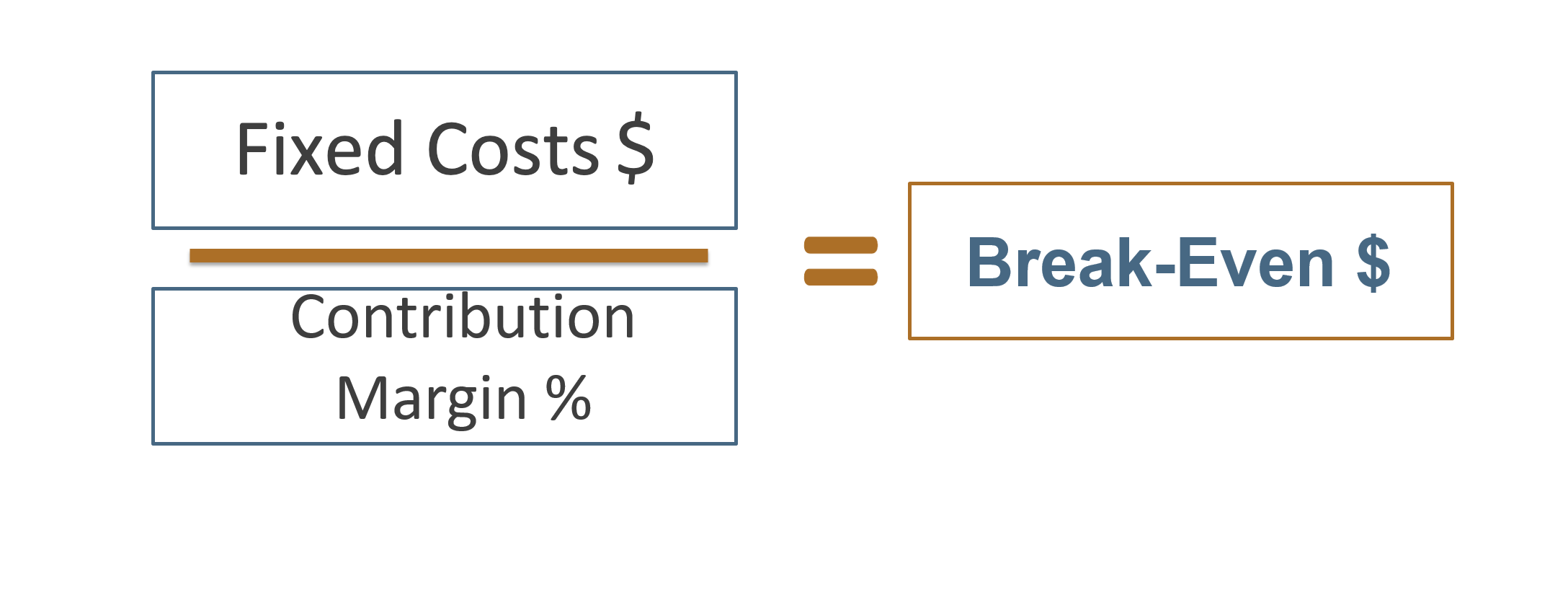

Cost-Volume-Profit Analysis

Taxes represent a portion of a company’s profit that must be paid to the government. Therefore, when calculating a target profit, it is essential to account for taxes, as they can significantly influence the final profit figure. Financial what is operating income operating income formula and ebitda vs operating income projections involve determining what level of profit you want from a business. However, profit is often assumed to be the end result, a natural consequence of setting revenue and expense levels in the financial projections.

Target Profit Calculation – Multiple Products

They need enough revenue to cover all their bills and still have money left over as profit. Based on last year’s volume numbers, the business forecasts to deliver 20 services over the year. Draw a line that represents the profit of P1 (the highest-ranked C/S product) scaled to the graph on the y-axis.

You might find yourself asking, “How can I predict whether my sales will hit that sweet spot where profits rise? ” This common plight can lead to missed opportunities and growth stagnation if not tackled head-on. The company wants to earn a profit of $80,000 for the first quarter of the year 2012. This allows businesses to assess whether they are on track to meet their goals, or an early warning signal if strategic adjustments are needed.

It means that Company ABC needs to sell 9,761 units to achieve a contribution margin of $ 585,714. So the company will be able to get a net operating income of $ 285, 714, and net income of $ 200,000. Understanding how to calculate target profit, analyze break-even points, assess sensitivity, and evaluate the impact of sales mix are essential components in this process. The target sales volume can be derived by tweaking the break-even formulae to incorporate the desired income. One of the helpful uses of CVP analysis is the determination of the sales required to generate a target profit (or desired income).

- To conduct a break-even analysis, businesses need to categorize their costs into fixed and variable components.

- Finally using the formula below the number of units it needs to sell to achieve the target profit level is as follows.

- Moreover, the sales mix can also impact resource allocation and operational efficiency.

- The company wants to earn a profit of $80,000 for the first quarter of the year 2012.

For instance, if a company has fixed costs of $50,000, a contribution margin of $10 per unit, and a target profit of $20,000, it would need to sell 7,000 units to meet its goal. Target profit analysis is a powerful financial tool that equips businesses with the ability to set and attain specific profit goals. By understanding the dynamics of contribution margin and break-even points, companies can develop strategies to reach their desired profit levels. Furthermore, the incorporation of taxes in this analysis ensures that profit figures are both realistic and actionable.

At the end of each month, the restaurant chain can compare the actual profits to the targeted profits, and assess the performance of each restaurant. Setting a target profit allows companies to factor in any potential market fluctuations, providing a safety net during uncertain times. On the other hand, if the target profit suggests cost-cutting measures, the business can explore areas for efficiency improvement.

Achieving profit requires controlling costs and achieving budgeted sales through this method. At the break-even point, profit equals zero, making it a critical reference point for businesses to gauge their financial stability. This equilibrium is achieved when the unit contribution margin, which is the profit contribution per unit sold, multiplied by the quantity sold, equals the fixed cost. Achieving target profit is a critical objective for businesses aiming to ensure long-term sustainability and growth.

Setting a target profit enables businesses to identify and mitigate financial risks by being aware of the factors that could potentially cause them distress. Setting a target profit helps the management allocate resources efficiently. Therefore, the business would need to sell 7,250 units to achieve their target profit. Again, setting the target profit to zero will give the sales break-even point. The first step is to determine the profitability of each product and rank them accordingly.